I was trying to understand why food startups are so hot when I ran across the following two charts.

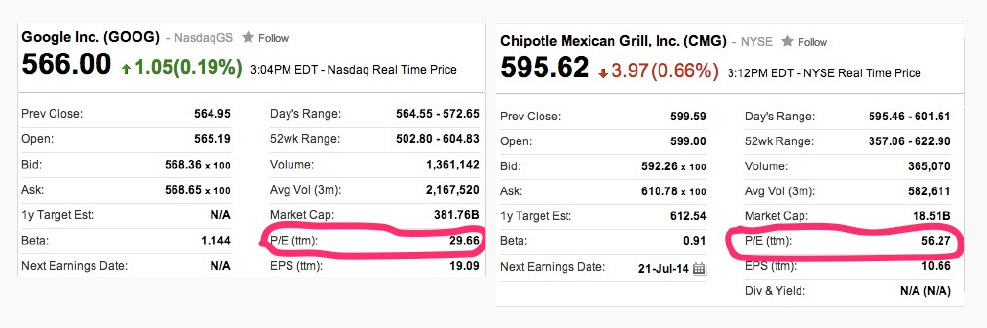

In the image, you’ll notice that I circled a line labeled “P/E.” In the language of finance, P/E is short for “price-to-earnings ratio,” which is the relative value of a company’s stock price to its profitability (aka earnings). When a company enjoys a high stock price yet barely turns a profit––like Amazon––it shows in the P/E ratio.

This typically happens when investors think the company will grow and reap huge profits down the road at some later date (or that someone else will pay an even higher price later on). Generally speaking, having a high P/E ratio means that investors like you and believe that you have a bright future.

The average P/E ratio on the major stock markets indices is 15. Google’s P/E ratio is 30. Chipotle’s P/E ratio is 56. Said another way: Chipotle’s profits are worth more than Google’s.

Mind. Blown.

Which brings me to the original inspiration for this post: Sprig.

Gagan Biyani, the founder of Sprig, is a friend of mine. Sometime last year we caught up and he told me about a new food delivery startup he was working on. They’d make the food themselves, he explained, and deliver it too — really fast.

Oof, I thought. Not a bad idea, but sounds like a tough sell to the capital markets. Lots of upfront cost, little relative profit, no clear customer lock-in or network effect. How would they ever join the 10x revenue club?

Since that conversation, Sprig has gone on to raise over $10 million from Greylock and others. Immediately, the floodgates opened: SpoonRocket raised $10 million.Munchery raised $28 million. Capital has literally flooded the food space, but I still didn’t get it. Why? What were the VCs seeing that I wasn’t?

At first glance, these companies reminded me of Postmates, which I classify as a premium service targeting a niche audience of wealthy urbanites willing to pay a 30 percent premium to have food delivered. How big could these businesses get, really, especially outside of the SF bubble? What the hell were investors thinking?

As I thought about it more, I realized that while Postmates and Caviar are services on top of restaurants, Sprig, Munchery and SpoonRocket are restaurants. Really, they’re the new fast food chains.

Like a Chipotle, these new fast food chains operate commercial kitchens, pay a chef to design their menu and hire low-skilled minions to mass-produce the actual food dishes. Unlike a Chipotle, these new fast food chains can lease out cheap real commercial real estate in out of the way, low-cost locations. Not only do the new fast food chains pay less per square foot of real estatec, they also need a fewer locations and thus less real estate in absolute terms. How many locations does SpoonRocket need to feed all of San Francisco? Three… maybe? Then think of Burger King — how many locations would they need to serve an equivalent volume of customers? Fifteen? Twenty?

And finally, instead of someone upselling you fries with that, the new fast food chains seal the deal with nice photography and a well-designed mobile app. Not bad efficiency.

Yet for the money they save on cashiers, the new fast food chains introduce a new, countervailing cost: human delivery agents. And with fuel costs being driven up by the rise of China’s middle class, delivery ain’t cheap — Sprig pays their SF delivery workers $16 an hour.

Software is eating food.

From an operations perspective, the relative costs of these inputs — real estate, food prep, delivery — are going to determine how profitable the new fast food chains are. The pressure to increase efficiency and drive down the costs in these companies will be great. For the workers on the other side of the iPhone app, the old industrial logic of low-pay-for-low-skill will apply just as it ever has, especially as more of the intelligence and skill becomes centralized in the form of software and the buffeting effect of venture capital goes away in five years or so when these companies mature.

Due to their vertically integrated operations, these companies can reimagine the entire value chain from the vantage point of software. They can apply A/B testing and innovative startup thinking to not just their website or mobile apps, but the entire food production and cooking process. Here, in the unglamorous backend of operations, is where the profits will be won or lost.

By way of comparison, the publicly traded stocks of the old fast food companies are kicking ass. In terms of P/E ratios, McDonald’s shares are doing better than Apple’s; Starbucks is beating the pants off of Facebook and nipping on the buds of Amazon.

How big can these businesses get? In a word, huge. By market cap, McDonald’s is a $100 billion business — that’s two-thirds of an Amazon. At $19 billion, Chipotle is worth a whole WhatsApp. Hell, Taco Bell’s parent company is almost worth one-and-a-half Twitters.

Whither the next unicorn(s)? Food. Trillions of dollars of consumption are quite literally in play.

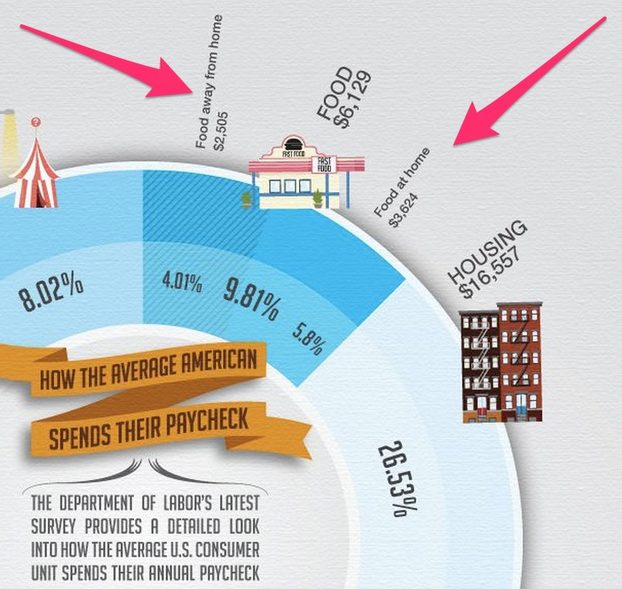

U.S. consumers spend $6,130 a year on food (~10 percent of all spending, depending how you slice it). And a dollar of Chipotle’s profit is worth more than a dollar of Google’s.

There will many winners. Unlike social networks or online marketplaces, there’s no winner-take-all dynamic in the food world. Homebrew’s Satya Patel summed up the typical VC mindset in his own explanation of why Homebrew is avoiding the food space, writing: “Many markets have room for more than one “winner” but very few have room for more than two or three.” Satya is wrong about food.

Food is a market like the Internet is a market — it’s too big to be to considered just one “market.” There’s high-end, low-end, middle of the road, Mexican, Sushi, Thai, Burgers, etc. The list goes on and on forever. Witness Jack in the Box ($2.4 billion), Panera Bread ($4 billion), Starbucks ($58 billion), Burger King ($9.4 billion), and more. The list of billion-dollar restaurant chains goes on and on, addressing all manner of market segments. Practically speaking, people don’t want to eat the same thing every day, thus supplier diversity is natural, organic and inevitable. And so it will be with the new fast-food chains who disrupt the old.

The food opportunity is so big because people need to eat three times a day. And unlike casual social interaction — here’s looking at you, Facebook — people happily pay for food. Counted in terms of DAUs, the number of potential daily active users for these companies is in the billions.

A thundering herd of food unicorns is assembling itself on the horizon. Prepare yourself. It’s not a fad. It’s not over yet. And you’re not too late.

This is just the beginning.

This post originally appeared in TechCrunch.

test